Stocks extended declines into a second week on continued signs of slowing global growth. Predominately negative economic data weighed on investor sentiment last week, culminating in Friday's weak payrolls report. The U.S. economy added 160,000 new jobs in April, the fewest in seven weeks. While the S&P 500 rose 0.32% on Friday, with investors reasoning that sluggish job growth lessened the likelihood of a June Fed interest rate hike, the benchmark index has retreated 2.2% since its recent April 20 high. The MSCI Emerging Markets Index lost 4.1% last week as investors withdrew $1.3 billion out of ETFs that invest in stocks and bonds in developing markets, ending 11 weeks of net inflows.

In key economic data last week, the Institute for Supply Management's PMI readings of manufacturing activity slowed for a second month in April, while construction climbed to its highest level in eight years. ADP Research said private payrolls rose the least in three years as service jobs rose below trend and manufacturing jobs declined.

For the week, the S&P 500 fell -0.33%, extending its two-week decline to -1.65%; the Dow Industrials slipped -0.19%; and MSCI EAFE dropped -3.03%.

What We’re Reading

Saudi Arabia Appoints New Oil Minister -- Reuters

Chinese Global Trade Contracts -- CNBC

Contrasting Leading Equity Indices -- CNBC

Chart of the Week: First Quarter GDP Not Great; See Downside Risks for Second Quarter

The What We're Reading economic report on a slowdown in Chinese international trade, particularly imports, has attracted some negative headlines, but this largely reflects seasonal distortions. Specifically, distortions around the timing of China's weeklong Lunar New Year holiday and a slump in commoditiy prices a year earlier. In contrast, volume data show commodity demand remains firm.

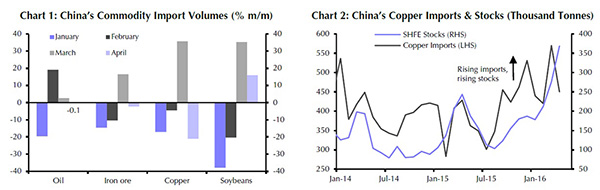

Data published over the weekend show China's total imports fell by 10.9% year-over-year (YoY) in US dollar terms in April, compared with a drop of 7.6% in March. Import volumes of all the main commodities, save soybeans, dipped, however this followed a surge in imports in March (see Chart 1).

Soybeans imports surged for the second consecutive month, despite the recent uptick in prices. Soybean crushing margins in China are high in part due to rising pork prices. However, given the weak start to the year, soybeans imports are still only up by 12% YoY in January-April. Meanwhile, copper imports slipped back in April, but were still 5% higher than a year earlier. The recent strength in imports has coincided with an accumulation of exchange stocks in China, suggesting that physical demand has not been growing as strongly (see Chart 2).

Export volumes of steel and aluminium also slipped back last month, but that followed particularly strong overseas sales in March. Overall, the April import data point to solid Chinese commodity demand. Imports could slip in the next month or so as stocks may be drawn down but, according to Capital Economics, they expect the cyclical pick-up in Chinese economic activity to translate into higher commodity import demand for the year as a whole.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.