U.S. stocks rose last Friday, sending the S&P 500 to a five-week high and its strongest weekly gain since March 4th. Equities recovered from a Friday dip sparked by a speech from Fed Chair Janet Yellen signaling a rate hike may be appropriate in "the coming months." Commerce officials said their second of three first quarter GDP estimates was upwardly revised to 0.8% from 0.5%, while on Thursday the Atlanta Fed's GDPNow forecast model for second quarter growth rose to 2.9% from 2.5%. The model adjusts its forecast with incoming economic data and officials said the increase came as private investment growth increased from -0.3% to 0.4% following a stronger-than-expected durable goods report.

After approximately two years in which speculation over the timing of rising interest rates has increased market volatility, investors are appearing more comfortable with the idea of a 2016 summer rate rise. Last week's biggest surprise in economic data was on Tuesday, when new home sales in April surged nearly 17% to the highest annualized level since the beginning of 2008. Durable goods orders for April jumped 3.4%, topping forecasts for 0.5% and followed a 1.9% March increase. Lastly, the University of Michigan's consumer confidence index rose less than forecast for May, as officials cited election concerns.

For the week, the S&P 500 gained +2.32%; the Dow Industrials advanced =2.13%; and the EAFE (developed International jumped +2.2%

What We’re Reading

Markets "Well Prepared" for Summer Rate Hike -- Reuters

Updated Odds for China A-Shares in MSCI Indices -- Reuters

India's Economy Grows Faster than Forecast -- Reuters

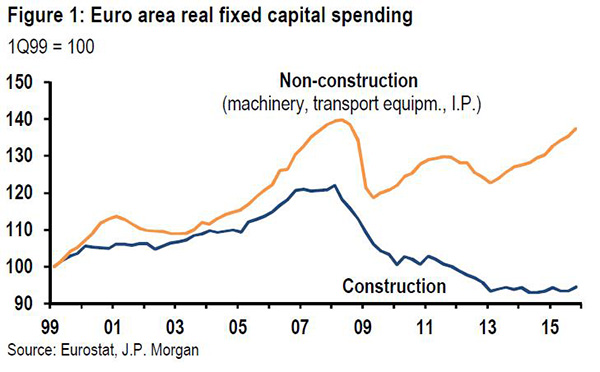

Chart of the Week: Euro-Area Capital Spending Slowly Recovers; Construction Side Drag Lessens

The recovery in the Eurozone's overall capital spending is gathering steam. Last year, capital expenditures (capex) grew at a 3.4% annualized pace, slightly faster than in the 1999-2007 period. There are two very different parts to European capex, with spending on machinery, transport equipment, and intellectual property recovering solidly. The "non-construction" spending has returned to the pre-2008 peak, grew by 5% last year, and is rising again as a share of the region's GDP.

In contrast, Eurozone construction spending finally has stabilized but, as the chart above shows, it is not yet contributing significantly to the euro-area's recovery. JPMorgan believes this may be because it was more overextended at the peak in 2007, at least when measured in nominal terms. There are tentative signs, however, that a turn in construction has begun. Both the construction confidence survey index and the construction PMI have been improving steadily over the past three years, while residential and commercial property prices have also been picking up.

For now, most of these signs point to only a modest turn. Yet given the very favorable financing conditions and significant scope for a cyclical recovery from low levels, the belief is there is a significant potential for the recovery in construction spending to strengthen.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.