Stocks finished lower during the Good Friday holiday-shortened week, with the S&P 500 breaking its five-week winning streak after previously recovering all of its 2016 losses. Investors' appetites began to fade after several Federal Reserve officials highlighted a case for raising interest rates sooner than generally expected. St. Louis Fed President James Bullard echoed Fed Chair Janet Yellen's call for at least two rate hikes this year, with the first coming as early as April perhaps. The hawkish view stirred US dollar strength, capping five consecutive daily gains, its longest rally since last April. Weakness on the Bloomberg Commodity Index on Wednesday and Thursday were its steepest back-to-back declines since February 2nd, prompting the first weekly declines in energy and materials shares since February 12th.

For the week, the S&P 500 fell -0.65%, the Dow Industrials slipped -0.49% and MSCI EAFE (developed international) declined -2.17%.

What We’re Reading

New Rate Hike May Soon Occur -- Reuters

India PM Modi Defends Growth Outlook -- Bloomberg

Chinese Industrial Profits Rebound -- CNBC

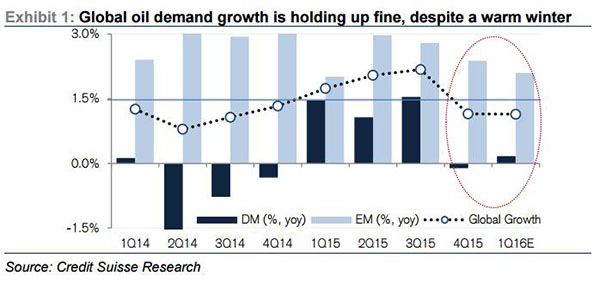

Chart of the Week: Global Oil Demand Still Alive; Supply & Demand May Balance in Coming Months

After a steep pullback in global oil demand starting in the third quarter of last year, the latest data supports the view that oil growth has not imploded and resilience remains strong. World oil growth decelerated in the final quarter of 2015, especially in North America, where diesel demand fell sharply due to slumping activity in mining and oil & gas drilling. Warmer winter weather across America also contributed. However, as the above chart shows, global oil demand grew by 1.2% in Q4 2015, with gains in Emerging Markets (EM) accounting for the bulk of the increase (+2.4%). Developed markets' oil demand growth detracted by 0.01% - mostly in the U.S. and Japan.

Moreover, early data for the current quarter does not look as bad as they did a month ago – February data either improved from January, with an increase in North America, or extended strong EM gains with Chinese oil growth appearing to have rebounded. Consequently, Credit Suisse has gained more confidence in their forecast that global oil supply and demand will rebalance in the next few months.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.