Stocks advanced on Friday, pushing all three major U.S. equity indices to a fifth straight weekly gain, their longest stretch of gains in five months. The Dow Jones Industrial Average and S&P 500 each completed one of the largest turnarounds in market history, erasing all losses incurred during the worst start to a year on record. In economic data last week, retail sales fell 0.1% in February, while sales excluding autos and gas rose 0.3%. Somewhat similarly, overall consumer prices contracted 0.2% last month, while core prices, excluding volatile food and energy prices, increased by 0.3%. Housing starts rebounded in February, up 5.2% to a 1.178 million annualized rate. The Philadelphia Fed's key manufacturing conditions survey index was strongly higher, jumping into positive territory, signaling the worst may be over for the factory sector.

For the week, the S&P 500 gained +1.37%, the Dow Jones Industrial Average advanced +2.26%, and EAFE (developed International) rose 1.01%.

What We’re Reading

Fed Chair Yellen Steers Fed Dovish -- Reuters

Oil Glut May Not be as Bad as Feared -- Bloomberg

China Central Bank Governor Warns on Debt -- Business Insider

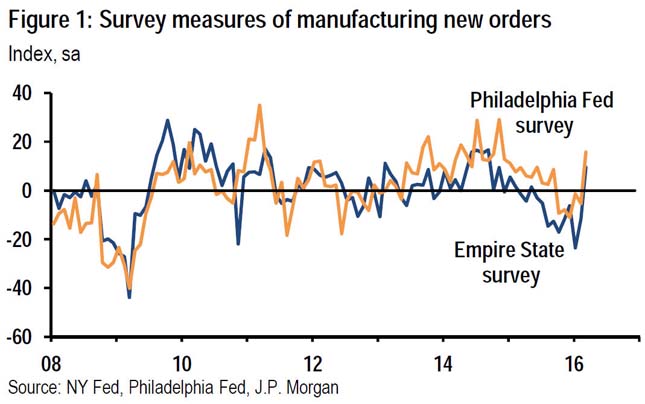

Chart of the Week: March Manufacturing See Solid Start; Importantly, Led by New Orders

The first two regional manufacturing surveys to report March data strengthened significantly during the month, turning positive for the first time this year. The headline level for the New York Fed's Empire State manufacturing survey surged 17-points to 0.62 in March, while the Philadelphia Fed's manufacturing survey leapt 15-points to 12.4. Perhaps more importantly, both surveys showed large increases for their measures of New Orders (seasonally-adjusted; see Figure 1 above). Impressively, New Orders on the Philadelphia Fed's survey rose to a positive 15.7 from negative 5.3 in February, as reported by Bloomberg. This is its first positive reading since September 2015.

A number of other manufacturing surveys will provide March data in the coming weeks, but the improvement in the two available to date signals that we are moving past the recent run of manufacturing weakness. It is likely that the largest drags from the stronger dollar and inventory correction may now be behind us.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.