Stocks finished lower last Friday, with the S&P 500 in retreat for a fourth day in the past five sessions. The S&P 500 ended with its worst weekly performance since April. Investors grew increasingly concerned about global growth ahead of the U.K.'s June 23 "Brexit" vote-a referendum vote to leave or stay within the European Union (E.U.). The debate turned violent when a gunman murdered Jo Cox, a British Member of Parliament and supporter of staying in the E.U. On Wednesday, U.S. Federal Reserve policy makers voted to keep interest rates unchanged and slightly reduced their gross domestic product (GDP) forecasts for this year and next. Fed Chair Janet Yellen acknowledged that the upcoming Brexit vote played a role in the Fed's decision to delay a rate hike. Also notable during the week, German 10-year sovereign debt yields turned negative for the first time in history.

For the week, the S&P 500 declined -1.12%; the Dow Jones Industrial Average fell -1.06%; and MSCI EAFE (developed international) lost -2.76%.

What We’re Reading

Brexit Polls Shift to "Remain" -- Bloomberg

Oil Rebounds, Nearing $50/barrel -- Reuters

Fannie Mae's View for Growth -- PRNewswire

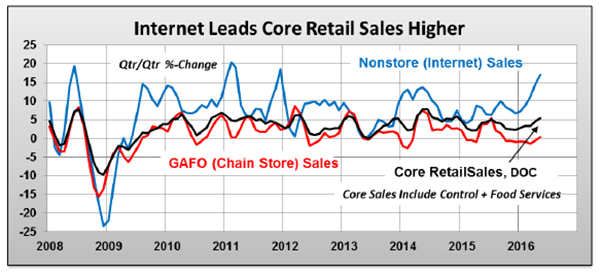

Chart of the Week: Retail Sales are Improving; Shopping Trends are Changing

After two soft quarters in monthly retail sales, the U.S. Department of Commerce's survey of retail sales surged 1.3% in April followed by a better than expected 0.5% gain in May. According to Argus Research, April and May retail sales are consistent with 5% or better current dollar growth in Personal Consumer Expenditures (PCE). Argus expects stronger sales growth in the second and third quarters, driven in part by a resurgence in internet spending, which has reached 4 ½ year highs. Specifically, the resurgence in core and control retail sales indicates that total consumer spending and GDP will be stronger in the second and third quarters. These factors could even play an important part in the Federal Open Market Committee (FOMC) policy deliberations regarding the timing of raising interest rates.

Traditional chain and department stores continue to lose market share, if not outright sales. Very few have been able to buck the trend. On the other side, however, non-store (Internet-based) retailers continue to amass sales and market share. As the chart above illustrates, Internet annual sales growth has doubled in the past 6 months, rising at a 17% rate in the past quarter. Core retail sales have bounced back to 5.4% in the 3 months ending in May, up from just 2.3% and 3.3% growth in Q4 2015 and Q1 2016. Core sales exclude auto, gas and building related. Control retail sales, which are Core sales less food services, also rebounded to 5.3% in the May quarter, up from just 1.3% and 2.8% reported growth in the fourth and first quarters, respectively.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.