Week of January 11, 2016

Optimism over Friday's better-than-forecast jobs report gave way to anxiety over sliding oil prices, global growth concerns and the timing of future Federal Reserve rate increases. The S&P 500 fell 1.08% on Friday, capping the week with a near 6% loss, its worst five-day start to a year on record. The week began with a weak PMI manufacturing reading out of China, sending the nation's Shanghai Composite down nearly 7%. Also last week, the People's Bank of China devalued its currency, sending the yuan down the most since its August 25 devaluation last year. Also contributing to investor angst, North Korea conducted a nuclear weapons test, claiming a successful detonation of its first hydrogen bomb. The Shanghai Composite slid 10% for the week, while the MSCI Emerging Market Index sank -6.81%. Europe's Stoxx 600 Index fell -6.69%, its worst weekly loss in four years.

For the week, the S&P 500 fell -5.91%, finishing at 1,922, its lowest level since September 30th. The Dow Jones Industrial Average shed -1,078-points, ending the week down 6.19%. While developed international stock indices fell -6.14%

What We’re Reading

Fourth Quarter Earnings Seasons Begins -- Bloomberg

Oil Prices at Lowest Since June 2004 -- Market Watch

China Growth Outlook Likely Not to Top 6.5%; -- Reuters

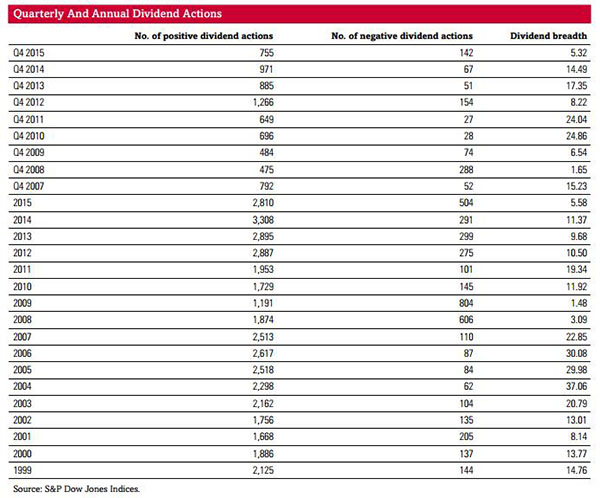

Chart of the Week: S&P 500 Dividend Payments Set a Record in 2015, Another Record Likely for 2016

On an overall basis, S&P 500 companies paid out 10% more in regular cash dividends in 2015 than in 2014, according to S&P Dow Jones Indices calculations. It was the fifth consecutive year of double-digit increases and the fourth record year for payments. From a quarterly perspective, payments for the fourth quarter of 2015 set a record, the seventh in a row. However, the quarter, with $3.6B in dividend net increases, showed a massive deceleration from the $12B increase registered during the fourth quarter of 2014. Energy issues accounted for 48% of the dividend cuts and 80% of the dollar cuts in this year's fourth quarter.

As this preceding chart illustrates, when reviewing the entire U.S. common stock universe (and not just the S&P 500), 755 dividend increases were reported during the fourth quarter of 2015, down from 971 increases reported during the fourth quarter of 2014, a 22.2% decrease. For all of 2015, 2,810 issues increased their payments, down from the 3,308 issues that increased their payments during 2014, a 15.1% decrease. Meanwhile, 142 companies decreased their dividends in the fourth quarters of 2015 (defined as either a decrease or a suspension) compared with 67 in the fourth quarter of 2014, a 112% difference. For all of 2015, 504 issues decreased their dividend payments, a large jump from 291 decreases in 2014, a 73.2% increase.

S&P Dow Jones Indices see two possible scenarios for 2016. On the pessimistic side, commodities would continue down as U.S. economic growth slows, and earnings would falter with a 0.75% (maximum) 2016 Fed increase—leaving dividend growth in the 3% area for 2016. On the optimistic side, oil and commodities would rebound slightly over the year (gyrating), and the economy would adjust to the Fed increase (1%-1.25%), inflation would pick up, especially in the second half of the year, consumers (though still selective) would spend more, and earnings would increase by low double-digits allowing dividends to increase roughly 8%-9% for 2016.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.