The S&P 500 advanced last week, completing its sixth weekly gain in the past seven weeks and finishing at its highest closing level of the year. The week was defined by a market-friendly speech delivered by Federal Reserve Chair Janet Yellen on Tuesday to the New York Economic Club, where she said she is in no rush to raise rates amid a sluggish global economy. Her stance that the Fed must "proceed cautiously" quashed rate hike expectations stirred by comments from several Fed district presidents that a rate hike could come as soon as April. The dovish stance helped equities conclude their largest quarterly turnarounds since the Great Depression.

The week culminated with continued gains in employment, with payrolls increasing by 215,000 in March, down slightly from an upwardly revised increase in February. Hourly earnings climbed more than expected, while the headline unemployment rate edged higher to 5% from 4.9% the month prior.

For the week, the S&P 500 rose +1.84%, the Dow Industrials gained +1.58% and MSCI EAFE (developed international) dipped -0.21%

What We’re Reading

ECB Begins Increased Debt Purchases -- Bloomberg

Dollar Falls on Yellen's Dovish Stance -- FX Street

New Doubts on Oil Output Freeze as Russian Oil Production Reaches 1987 High -- Marketwatch

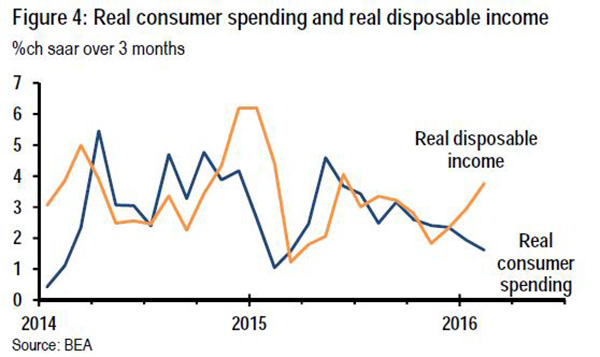

Chart of the Week: The Consumer Spending Conundrum; Incomes Rise, Spending Slows

The chart above shows real consumer spending increased at a moderate 0.2% seasonally-adjusted monthly rate in February, but the January figure was revised lower to unchanged from 0.4%. This in turn reduced the tracking estimate of 1Q 2016 real consumer spending growth from 2.9% to just 1.7% (seasonally-adjusted annual rate, SAAR). January real spending on goods was revised down to minus 0.3% (from +0.7%) and spending on services was revised down to +0.1% (from +0.3%).

On the other hand, real disposable income, through the first two months of the quarter, was up a solid 3.4% (SAAR), so the slowdown in spending reflects an abrupt increase in the saving rate, from a 5% average in 4Q 2015 to 5.4% in February. Unfortunately, there is no obvious reason for the spending slump, although the sharp decline in equity prices early in the year may have discouraged spending. If this is the case, then we would expect a rebound in spending relatively soon. However, data on Friday showed unit auto sales were tracking at 16.6 million for March, down from 17.4 million the month before and the weakest pace since February 2015. Confounding matters further, auto makers spent an average of $3,110 on sales incentives per vehicle sold last month, 14% more than a year earlier and up slightly from February, according to Autodata Solutions.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.