Equities sold off globally last Friday, giving back most of the gains of the prior week, on news that the U.K. referendum on European Union (E.U.) membership ended with a vote to leave the union. The Dow Jones Industrial Average retreated by over 600 points (-3.39%) from Thursday's highs and the S&P 500 lost 75 points (-3.59%), erasing most of the year's gains for the U.S. equity gauges. European and Japanese stocks fared worse, falling by over 7% on the day, while Hong-Kong equities lost 2.92%. We should note that much of the losses appear oversized because of the rally that had occurred in the early part of the week, and on a week-to-date basis, declines were in the 1.5% to 2% range with international stocks lagging slightly.

There is still much that is not known on how Britain's situation will resolve itself, and while we may see some additional volatility, on Friday the markets were largely back to levels of about a week ago, suggesting this is a reaction to a localized negative event rather than a global crisis.

For the week, the S&P 500 declined by -1.62%; the Dow Jones Industrial Average fell -1.55%, and MSCI EAFE (developed international) lost -1.73%.

You Can Read our Full Commentary on Brexit Here

What We’re Reading

U.K. PM Cameron: No Do-Over Brexit Vote -- Bloomberg

Treasury Secretary Lew Sees No Financial Crisis from Brexit -- Reuters

UK Loses AAA Credit Rating -- CNN Money

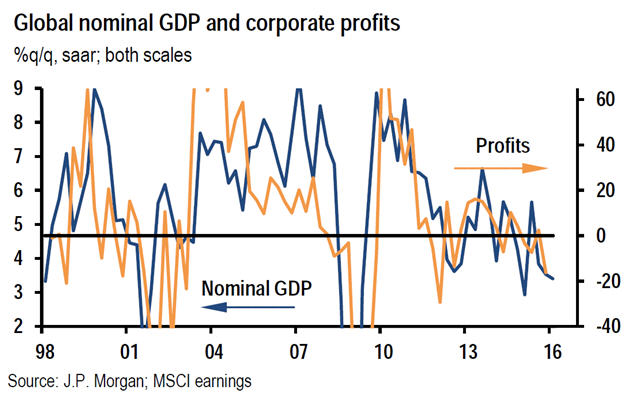

Chart of the Week: You Picked a Fine Time to Leave, U.K. - Global GDP and Corporate Profits are Under Stress

While the global economy has delivered disappointing growth in recent years, it has remained bounded close to its trend pace, highlighting its resiliency in the face of a number of global shocks. However, JPMorgan has forecast that global growth could decline by roughly 0.2% as a result of Brexit, and it should be viewed as a continuation of this disappointing but resilient performance. That said, financial market and sentiment spillovers from this policy-induced drag on European growth comes at a time in which there are important vulnerabilities. As seen in the chart above, global corporate profits are contracting.

In developed markets, the U.S. corporate sector is under particular pressure, as external drags from an elevated dollar and low oil prices combine with weak productivity gains. This drag has produced a contraction in investment and slowing in job growth. Our forecast assumes the profit drag will fade, due to a stable dollar and higher commodity price, and that solid gains in consumer spending will buoy corporate confidence. The risk is that Brexit magnifies the pullback through a stronger U.S. dollar and rising global uncertainty. In response, JPMorgan lowered its second half 2016 U.S. GDP growth forecast from 2.3% to 2%.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.