U.S. stocks slumped last week, snapping two weeks of gains, as a mixed January jobs report and disappointing earnings sent consumer and technology shares sharply lower. The NASDAQ Composite Index finished at its lowest level since October 2014. The latest sign of weakness among a tier of momentum stocks stirred concerns that sluggishness may be broadening. At the same time, new economic data showed slowing growth in the service industries, along with manufacturing. Labor officials said employers added 151,000 new jobs last month, shy of forecasts for 190,000. And while the unemployment rate declined to 4.9%, a jump in wage growth sent the dollar higher, renewing Wall Street uncertainty about the pace of future interest rate hikes.

For the week, the S&P 500 retreated -3%, the Dow Jones Industrial Average lost 261 points, or -1.6%, while the MSCI EAFE (Developed International) sank -1.52%.

What We’re Reading

Dollar/Yen Falls to 15-Month Low -- Reuters

Venezuela Seeks Global Cooperation on Oil Production - Reuters

Puerto Rico Appeals to Congress for Restructuring -- New York Times

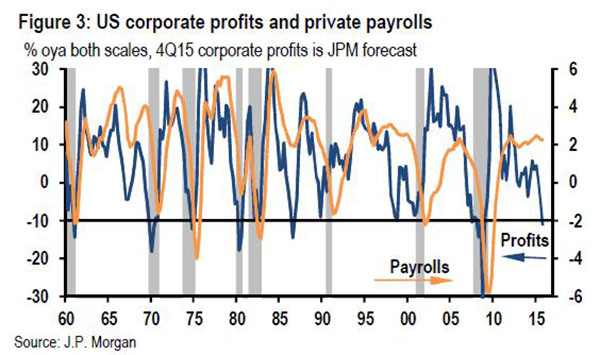

Chart of the Week: U.S. Corporate Profits Get Squeezed; Recession Odds Ratchet Higher

J.P. Morgan's global Purchasing Managers Index (PMI) survey drifted just 0.2% lower last month, but at 52.5 the index remains close to its average for the current expansion. However, the squeeze on U.S. profit margins is most severe and downside risks are the greatest since the 2008-2009 financial crisis. Along with the dollar's 21% cumulative rise since mid-2014, the U.S. is a significant energy producer, under siege with collapsing world oil prices. At the same time, stagnant worker productivity has produced sufficient labor market tightening to move wage inflation modestly higher. Against this backdrop, this past week's larger-than-expected productivity drop in the fourth quarter of 2015 points to a 10% drop in corporate profits from year-ago levels. A double-digit decline in profits is a rare event outside recessions, having been recorded only twice in the last half century (see Figure 3).

In sum, global PMI activity data provides comfort that underlying global growth momentum has not meaningfully downshifted. However, with the drag on U.S. earnings intensifying and business spending softening, the risks of a broader business pullback remain elevated. J.P. Morgan's U.S. recession tracker that measures the probability of a recession within 12 months increased to just under 25% from 15% at the beginning of the year.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.