U.S. stocks slipped on Friday, slightly trimming a second straight weekly gain, after a pickup on the Fed's preferred measure of inflation overshadowed a surprise upward revision on fourth quarter gross domestic product (GDP) growth. The personal consumption expenditures (PCE) inflation rate, along with its core measure, both rose more than expected in January, up 1.3% and 1.7% year-over-year respectively. Commerce officials said their second (of three) fourth quarter GDP estimate grew to 1% annualized, up from an initial 0.7%. Economists' consensus forecast called for downward revision to 0.4%. The S&P 500 has advanced over 6.5% in the two weeks since reaching a 22-month low on February 11.

In other key economic data last week, Markit Economics' Manufacturing Purchasing Managers' Index (PMI) fell to 51 for February—a three-year low. However, it remains above the 50 level, which is regarded as the dividing line between growth and contraction. The S&P/Case-Shiller 20-city home price index rose 0.8% in December, capping 2015 with a 5.7% increase, matching November as the highest 12-month gain since July 2014.

For the week, the S&P 500 gained +1.63%; the Dow Jones Industrial Average rose +1.51%; while the EAFE added just +0.15%.

What We’re Reading

Friday's Jobs Report for February Becomes Pivotal -- MarketWach

Crude Oil Shows Signs of Stabilizing -- Reuters

G-20 Produces No Sweeping Growth Initiatives -- Reuters

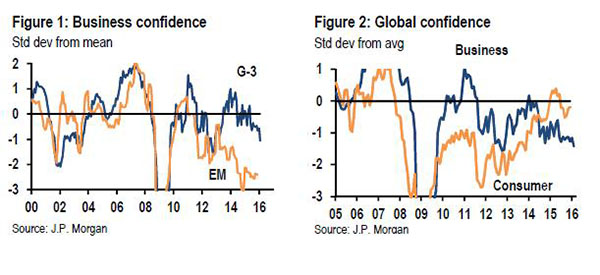

Chart of the Week: Downside Tail Risk Concerns Are Shifting From Emerging to Developing Markets

For some time now, J.P. Morgan's (JPM's) economic forecast has incorporated elevated concerns about negative tail risks to global growth. However, the source of these concerns has shifted. Risks of a China hard landing or a disruptive emerging market (EM) credit deleveraging persist, but they have not intensified in recent months. Indeed, we have seen encouraging signs that Chinese growth is stabilizing and policies look set to stimulate credit and infrastructure spending. Instead, the focus of downside risk has intensified on developing markets (DM).

While the recent tightening in financial conditions contributes to this shift, JPM doesn't believe the overall thrust of financial conditions, netting out movements in equities, credit, oil, and interest rates, is generating a significant drag yet. However, DM GDP growth slowed sharply and broadly last quarter with Japan contracting and U.S. and Euro area growth at just 1%. Some may see this slowdown as transitory, following the pattern of choppy but above-trend DM growth over the past two years. However, signs are present that indicate a more significant behavioral shift may now be taking hold.

Economists are concerned that DM businesses may respond to the squeeze on their profits with a further slowing in capital spending and a pullback in hiring. This past week's February readings pushed business confidence down to the lowest level since late 2012, at the height of the Euro area debt crisis (see Figure 1 above). While developing and global business confidence has turned lower, we are fortunate that global consumer sentiment has most recently been on a rebound (see Figure 2). Lastly, and also favorable, the evidence on DM labor markets remains positive. Economists' consensus forecast for February payrolls, due to be released this Friday, looks for an increase to 195,000 from January's slowdown to 151,000. Let's hope they are right.

Articles chosen and summarized by the Cetera Investment Management team. Cetera Investment Management provides investment management and advisory services to a number of programs sponsored by First Allied Securities and First Allied Advisory Services. Cetera Investment Management individuals who provide investment management services are not associated persons with any broker-dealer. International investing involves additional risk, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in companies involved in one specified sector may be more risky and volatile than an investment with greater diversification.